Variable overhead costs decrease as production output decreases and increase when production output increases. If there is no production output, then there would be no variable overhead costs. Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Manufacturing overhead includes items such as indirect labor, indirect materials, utilities, quality control, child adoption costs credit material handling, and depreciation on the manufacturing equipment and facilities, and more. Fixed manufacturing overhead costs are indirect costs that remain constant regardless of changes in the production volume, such as rent, insurance, and supervisory salaries. Manufacturing overhead is added to the units produced within a reporting period and is the sum of all indirect costs when creating a financial statement.

What is Variable Overhead?

Another example is the cost of the manufacturing supplies (such as needles and thread) that increase when production increases. We will assume that these variable manufacturing overhead costs fluctuate in response to the number of direct labor hours. The three primary components of a product cost are direct materials, direct labor and manufacturing overhead. Manufacturing overhead is a catch-all account that includes all manufacturing costs a business incurs other than direct materials and direct labor.

Understanding the High-Low Method for Cost Estimation in Business Finance

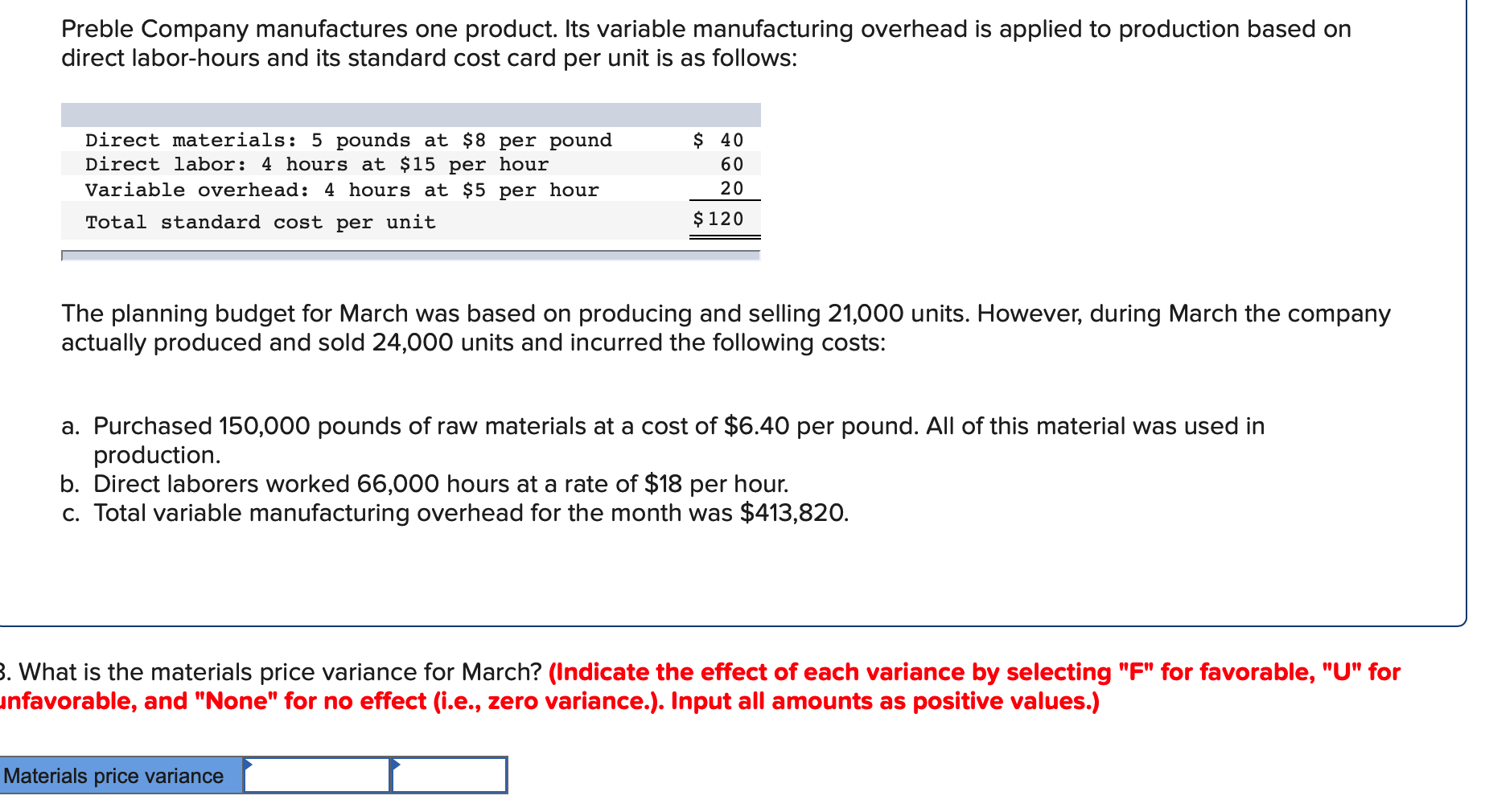

- The variable overhead efficiency variance calculation presentedpreviously shows that 18,900 in actual hours worked is lower thanthe 21,000 budgeted hours.

- Get reports on project or portfolio status, project plan, tasks, timesheets and more.

- Manufacturing overhead includes items such as indirect labor, indirect materials, utilities, quality control, material handling, and depreciation on the manufacturing equipment and facilities, and more.

- Are variable manufacturing overhead expenses included in your standard costs budgets?

Get reports on project or portfolio status, project plan, tasks, timesheets and more. All reports can be filtered to show only the cost data and then easily shared by PDF or printed out to update stakeholders. You can find the overhead rate of your manufacturing operations using the following formula. These physical costs are calculated either by the declining balance method or a straight-line method. The declining balance method involves using a constant rate of depreciation applied to the asset’s book value each year.

Understanding Variable Manufacturing Overhead: Components, Calculation, and Management

As a result, this is an unfavorable variable manufacturing overhead efficiency variance. Most manufacturing overhead budgets cover a year, but each of these values are calculated quarterly. The activity base chosen should have a strong correlation with the overhead costs incurred. For instance, if electricity consumption increases linearly with machine usage, machine hours might be the most appropriate base. A company may even use both machine and labor hours as a basis for the standard (budgeted) rate if the use both manual and automated processes in their operations.

Predetermined Manufacturing Overhead Rate Formula

Now let’s assume that the actual cost for the variable manufacturing overhead (electricity and manufacturing supplies) during January was $90. Some examples of variable manufacturing overhead costs are the cost of utilities such as electricity, water or fuel to operate machinery and supplies such as protective equipment or sales commissions. A manufacturing overhead budget covers all fixed, variable and applied manufacturing overhead costs of an organization.

Semi-Variable Overhead Costs

The higher the percentage, the more likely you’re dealing with a lagging production process. Manufacturing overhead is the sum of all the manufacturing costs except direct labor or direct materials costs. You can calculate applied manufacturing overhead by multiplying the overhead allocation rate by the number of hours worked or machinery used. So if your allocation rate is $25 and your employee works for three hours on the product, your applied manufacturing overhead for this product would be $75. The labor involved in production, or direct labor, might not be variable cost unless the number of workers increases or decrease with production volumes.

Within manufacturing overhead, some costs are fixed — meaning, they don’t tend to change as production increases — and others are variable. Variable manufacturing overhead costs differ based on how much the company produces. Before production begins, a business will typically calculate a standard or estimated variable manufacturing overhead for the year. Accountants come up with this figure by analyzing historical data and determining how much variable overhead expense the company tends to incur per unit produced. For example, if variable overhead costs are typically $300 when the company produces 100 units, the standard variable overhead rate is $3 per unit.

Conversely, companies with more variable costs than fixed might have an easier time reducing costs during a recession since the variable costs would decline with any decline in production due to lower demand. Cost behavior refers to the way in which a cost changes in relation to changes in the level of business activity or volume of production. This variance is unfavorable for Jerry’s Ice Cream becauseactual costs of $100,000 are higher than expected costs of$94,500. Variable overhead is typically aggregated into the cost of goods sold, and so is not shown separately in the income statement. However, it may be listed as a separate line item in the cost of goods manufactured schedule, which is internal to the accounting department; it is not included in a company’s financial statements. There are many costs that occur during production that it can be hard to track them all.

For example, you can use the number of hours worked or the number of hours machinery was used as a basis for calculating your allocated manufacturing overhead. To calculate manufacturing overhead, you have to identify all the overhead expenses (like the three types mentioned above). Sometimes these are obvious, such as office rent, but sometimes, you may have to dig deeper into your monthly expense reports to understand what’s happening. The forensic accountant who investigated thefraud identified several suspicious transactions, all of which werecharged to the manufacturing overhead account.

A company that has production runs of 10,000 units and a cost per unit of $1, might see a decline in the direct cost to 75 cents if the manufacturing rate is increased to 30,000 units. If the manufacturer maintains selling prices at the existing level, the cost reduction of 25 cents per unit represents $2,500 in savings on each production run. Explore the intricacies of variable manufacturing overhead, including its elements, cost implications, and effective management strategies for businesses. For instance, rent and insurance on a factory building will be the same regardless if the factory is churning out a lot or a little in terms of quantity. Variable overhead, however, will increase along with the amount produced, such as raw materials or electricity.